The Management Discussion and Analysis (MD&A) part of a company’s annual report explains company performance and productivity. This is generally undertaken by senior management and bsuiness analystsa that are tasked with analysing the company’s performance through both qualitative and quantitative data.

What’s included in the Management Discussion and Analysis?

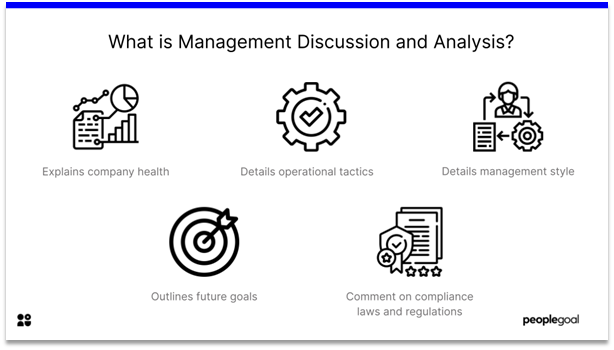

Whilst all sections of an annual report unveil useful information, the MD&A is crucial. The MD&A tells shareholders the reasons why a company is healthy, or the reasons why it’s not. The MD&A interprets the numbers in the financial statements; it details operational tactics and the management style that has led the company to its current state. It outlines future goals and looks ahead to new projects. Fundamental analysts should review a company’s Management Discussion and Analysis when considering an investment opportunity. Investors need to remember that this section is unaudited, unlike the financial statements.

As well as providing commentary on financial statements, the MD&A will also comment on compliance with laws and regulations, systems and controls, as well as actions that have been planned in order to tackle any obstacles the business may be facing. In America, it is just one of many sections required by the Securities and Exchange Commission (SEC) and the financial Accounting Standards Board (FASB) to be included in a public company’s annual report to shareholders. This allows any potential investors to understand the company’s financial fundamentals and management’s thinking, beliefs, and performance.

Key Aspects of the Management Discussion and Analysis

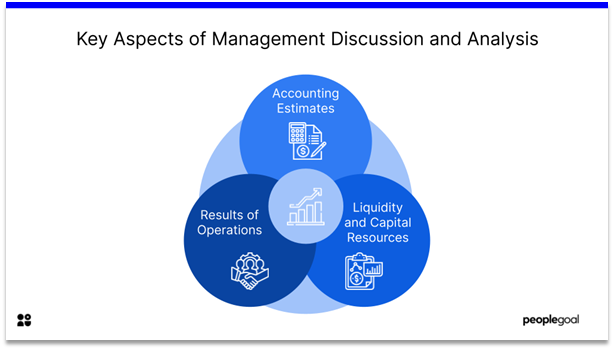

These are just three key areas of the MD&A, and organizations will add many more depending on their line of business.

Critical Accounting Estimates

In order for investors to fully understand the effects of accounting policies and any judgements made when implementing the policies, the SEC encourages companies to fully divulge their accounting policies within their MD&A.

Liquidity and Capital Resources

Part of the MD&A is management’s responsibility to identify any known trends, events, demands, or uncertainties that are likely to result in material changes in liquidity or capital resources. This area of the report should also include information on the company’s material commitments for capital expenditures and any anticipated sources of funds to meet such commitments.

Results of Operations

When reporting on the results of operations, the management must focus on unusual events or transactions and any significant economic changes that have affected income from continuing operations. Any trends or uncertainties that have occurred or that they expect to have an impact on the net revenues from operations, whether it be positive or negative, must be explained. In the case of the company having a significant rise in sales or revenues compared to previous periods, management must ascertain the degree to which the increase is attributed to operational change, the introduction of a new product or service, a price increase, or to some other factors.

Ready to 3x Your Teams' Performance?

Use the best performance management software to align goals, track progress, and boost employee engagement.

![What Is Employee Performance Management? [Tips to 3x Productivity]](https://www.peoplegoal.com/blog/wp-content/uploads/2019/08/What-Is-Employee-Performance-Management_.png)